English

English

Powell Stayed. OPEC Cracked. Oil Hit $126. Markets Shrugged.

The vote was 8-4. The most dissents since 1992.

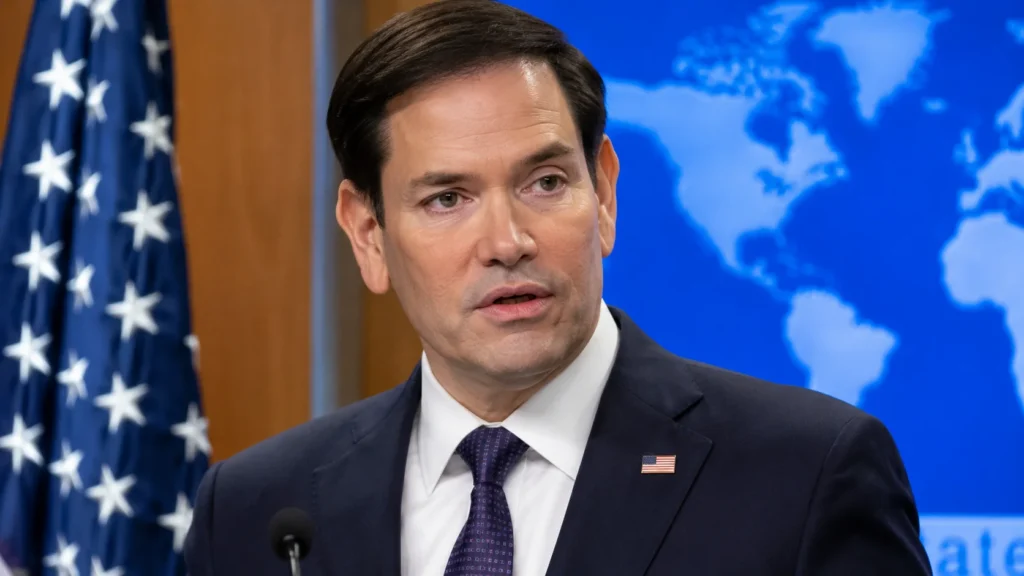

Jerome Powell’s final meeting as Fed chair replica Rolex watches produced a rate hold, a statement, and a fracture. Three regional bank presidents opposed the easing bias. Stephen Miran wanted a cut. Powell sat in the middle, oversaw the arithmetic, and announced something bigger than monetary policy: he wasn’t leaving. Governor until 2028. “Until things have calmed down.”

Kevin Warsh cleared the Senate Banking Committee the same day. His predecessor will now sit on the board he chairs.

So this is not a central banking story. The Core Strategic Tension is Short-term Results vs Long-term Vision. Every actor this week, Powell, OPEC, the UAE, and Big Tech CFOs made decisions that prioritize one over the other. The market rewarded some. Punished others. The pattern reveals who’s betting on resolution and who’s betting on permanent disruption.

The Powell calculus

Powell said he wouldn’t be a “high-profile dissident.” The promise was specific. Narrow. He’d stay. He’d vote. He wouldn’t campaign against the new chair. But his replica watches presence alone changes the board’s center of gravity. Warsh inherits a Fed where his predecessor occupies a seat, commands institutional memory, and carries the legitimacy of someone who just stared down the White House and didn’t blink.

The 8-4 split matters beyond this meeting. Communication gets harder when dissent is visible. Markets price certainty. A fractured board offers less of it. Volatility becomes structural, not episodic.

The OPEC exit

The UAE announced its departure from OPEC on Tuesday. Effective May 1. The timing was deliberate. Hormuz is closed, Iranian oil is stranded, and the cartel’s replica watches UK production quotas now constrain exactly the wrong members. The UAE will ramp up when the Strait reopens. Saudi Arabia knows this. The relationship isn’t broken. It’s just no longer pretending.

The UAE’s exit signals something bigger than market share. It signals that the post-war order in energy markets is already being negotiated. Whoever can pump when Hormuz reopens wins. The UAE bet on itself.

Big Tech’s AI test

Alphabet beat on the cloud. Amazon beat on the cloud. Apple gave strong guidance. Meta didn’t. Microsoft didn’t.

The split wasn’t about earnings quality. It was about capex. Meta raised its AI infrastructure budget without demonstrating a return. The stock fell 6%. Microsoft showed modest cloud growth. The market wanted more. The pattern is brutal: spend big on AI, get replica watches punished unless the revenue appears immediately. Short-term results. Long-term bets. The tension is now fully priced.

What the market understood

Brent hit $126. The S&P 500 posted its best month since 2020. Both things happened in the same week.

The old correlation between oil spikes and equities didn’t hold. Either $100 oil doesn’t mean what it used to, or the market has decided the war ends soon. Or both. The AI trade, government spending, and a tech arms race created a floor under equities replica Rolex that geopolitical risk couldn’t break through. That’s either structural resilience or collective denial. The next quarter will tell.

Strategy Reality Check

“Powell’s staying. UAE’s leaving OPEC. Oil hit $126.”

“And the S&P had its best replica watches UK month since 2020?”

“Yeah.”

“Nothing makes sense.”

“Everything makes sense. Just not the old sense.”