English

English

Iran War Energy Shock Disrupts Global Oil Markets

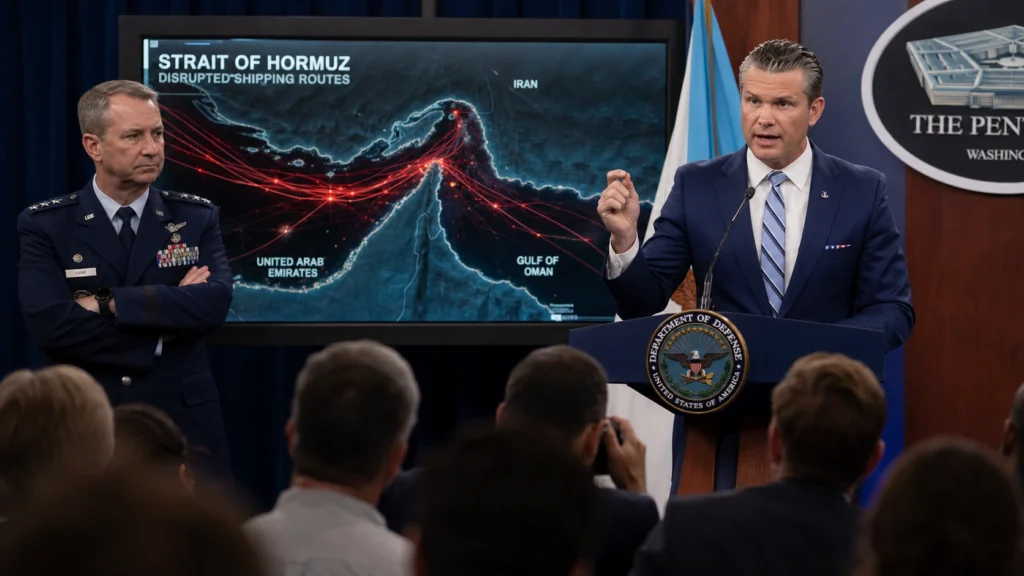

The Iran war energy shock is now reshaping global oil markets as the United States confirms $29 billion in conflict-related costs on 13 May 2026. The Pentagon update, delivered by Comptroller Jay Hurst, comes as oil traders react to rising Middle East risk, tighter shipping conditions near the Strait of Hormuz, and growing pressure on global inflation. The conflict now sits at the intersection of military escalation, energy pricing, and supply chain instability, with China’s dependence on Iranian crude adding further geopolitical weight.

Oil markets react before policy does

Brent crude briefly crossed $100 per barrel on 12 May 2026, according to the International Energy Agency (IEA). The movement did not follow a production cut. It followed risk repricing. Traders adjusted exposure to Middle East shipping lanes as conflict signals intensified.

The US Energy Information Administration (EIA) raised its 2026 gasoline forecast to $3.88 per gallon, citing volatility linked to geopolitical instability. That adjustment shows how energy shocks now flow directly into consumer inflation expectations instead of staying confined to commodity markets.

What changed in the past two months

In March 2026, maritime insurance premiums for tankers crossing the Gulf increased after a series of Iran-linked security incidents, according to Lloyd’s Market Association briefings. That shift raised baseline shipping costs across Asia and Europe.

By April 2026, Harvard Kennedy School economist Linda Bilmes estimated the long-term fiscal exposure of the conflict could reach $1 trillion once indirect costs like veterans’ care, infrastructure repair, and energy-driven inflation are included.

On 13 May 2026, Pentagon comptroller Jay Hurst confirmed direct US spending had reached $29 billion, up from $25 billion just two weeks earlier.

These numbers move independently, but they connect through one channel: oil pricing.

Fragment. The market saw it first.

Energy pressure is now structural, not temporary.

The Iran conflict is no longer operating as a contained regional war. It sits inside a global energy system already constrained by limited spare capacity.

OPEC+ maintains disciplined output levels, leaving global spare capacity below 3 million barrels per day, according to official OPEC production data (https://www.opec.org). That limit reduces the system’s ability to absorb shocks quickly.

US military operations add indirect pressure through fuel logistics, carrier deployments, and procurement of energy-intensive systems. At the same time, China’s reliance on Iranian crude stabilizes Tehran’s export revenue, linking Asian energy demand directly to Middle Eastern risk.

Energy dependency now acts as leverage. Not policy.

Who gains and who absorbs the pressure

Washington retains military reach, but fiscal predictability weakens as operational costs rise. Each escalation feeds domestic inflation through fuel-linked pricing channels.

China gains indirect influence. Its crude imports from Iran keep a revenue channel open even under sanctions pressure and regional instability. That influence remains quiet but structurally important.

Iran sits at the center of volatility. Even limited disruption in shipping lanes forces global buyers into hedging behavior, raising global price sensitivity.

As previous geopolitical risk analysis on supply chain resilience has shown, modern conflicts no longer end at ceasefire lines. They extend into pricing systems, insurance markets, and inflation cycles.

Expert view

Dr. Robin Brooks, former chief economist at the Institute of International Finance, said in a 2026 briefing that “energy markets now transmit geopolitical shocks faster than policy institutions can respond.” He linked current volatility to layered risks across shipping, sanctions, and fiscal exposure.

What happens next

The next major pressure point sits in maritime insurance pricing across the Strait of Hormuz. If insurers raise premiums again, shipping costs will ripple into European and Asian inflation within weeks.

Key indicators to watch include OECD oil inventories, OPEC+ compliance levels, and US-China diplomatic language around “energy stability.”

Slow movement first. Then a sudden adjustment.

Author

Written by an international economics and geopolitical analyst with over 10 years of experience covering energy markets, Middle East conflict dynamics, and global trade systems.